“There is a new world order,” Vice President JD Vance recently declared. “There is a new world order in trade; there is a new world order in globalization.”

The shift away from the old US-led order is visible in tariff schedules, export controls, energy contracts, investment screening, and trade agreements being built outside the old free-trade consensus. For decades, globalization was sold as a system of American hegemony, open supply chains, and the belief that economic integration would soften political rivalry. China was the ultimate test of that theory. China became richer without becoming Western. Washington’s answer has not been a return to free trade, but the construction of controlled commerce.

Goods still move, firms still seek markets, and governments still negotiate agreements. What is dying is the idea that trade should be governed primarily by consumers, producers, and prices rather than ministries, security agencies, and negotiated quotas. Free trade is becoming ever more rigidly controlled: managed by states, shaped by security concerns, and increasingly organized through political blocs rather than universal rules of open exchange.

The Bipartisan Turn Against Free Trade

The bipartisan turn away from free trade has been a public-policy blunder that favors politically protected industries while neglecting consumers. That is the snowball effect of government intervention: tariffs generate retaliation, retaliation justifies subsidies, subsidies create managed purchase agreements, and managed agreements necessitate new boards, exemptions, and political bargaining.

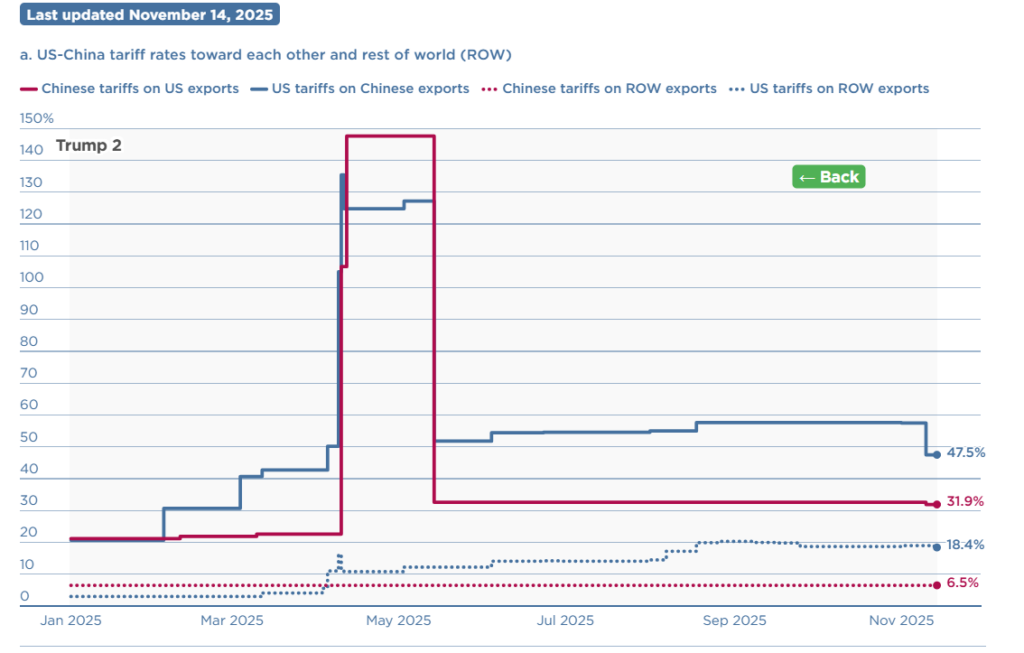

The US–China trade war began under Trump in 2018, remained largely intact under Biden, and has escalated further in Trump’s second term. The contrast is striking: while China lowered its average tariffs on the rest of the world from 8.0 percent in early 2018 to about 6.5 percent by early 2022, the United States raised its average tariffs on the rest of the world from 2.2 percent in January 2018 to 18.4 percent today.

According to PIIE, average US tariffs on Chinese goods stand at 47.5 percent and cover all imports from China, while China’s average tariffs on US goods stand at 31.9 percent. This is no longer temporary leverage. It is structural protectionism.

The stated justification for tariffs was that they would revive domestic manufacturing. The manufacturing numbers tell a different story. FRED reports that US manufacturing employment stood at 12.596 million in April 2026. That figure remains far below the old industrial-employment base invoked by “Made in America” rhetoric. Tariffs can make industrial revival sound muscular, but they cannot recreate the manufacturing economy of the late twentieth century. Consumers, meanwhile, pay the costs long before the promised factories arrive, if at all.

Roughly a year after Trump’s so-called “Liberation Day” tariff push, the results remain underwhelming: more federal involvement, more uncertainty, and no return to the industrial employment base politicians promised. The contradiction becomes clearest in Washington’s latest China policy.

Managed Rivalry, Not Free Trade

The current US-China arrangement shows controlled commerce in practice. The White House presented President Trump’s China summit as a historic breakthrough. China agreed to purchase 200 Boeing jets, with Trump suggesting the order could eventually rise to 750 aircraft. Treasury Secretary Scott Bessent stated, “We’re going to talk about a ‘Board of Investment’ that will be responsible for investment in non-sensitive areas.”

A second joint organization is in the making, with the White House Fact Sheet stating, “The Board of Trade will allow the United States Government and the Government of China to manage bilateral trade across non-sensitive goods.” On its face, this looks like a diplomatic victory for American manufacturing and global stability. Beneath the triumphal language, however, sits a more revealing reality. This is not free trade, and it is not market competition. It is state-managed bargaining between rival great powers, a cartel logic applied to global commerce.

Nor was Boeing alone in revealing how corporate access now depends on state diplomacy. Aircraft sales are not being left to open markets alone. They are being negotiated by heads of state, bundled into a broader geopolitical relationship, and tied to questions of supply chains and bilateral stability. The visit, the first by a sitting US president to China in nearly a decade, brought a large corporate delegation to Beijing, including executives from Apple, Tesla, Goldman Sachs, Boeing, Cargill, Visa, Citigroup, Nvidia, BlackRock, and Blackstone. The presence of these firms reveals the contradiction that tariffs promised to bring production home — but the summit was organized around preserving corporate access to China.

Agriculture shows the same absurdity. In the early trade war, China turned soybeans into a political weapon: after Washington imposed tariffs in 2018, Beijing responded with a 25 percent retaliatory tariff on US soybeans, and US soybean exports to China fell by $9.1 billion that year. A partial recovery in the same sector is being repackaged as a diplomatic victory. US Trade Representative Jamieson Greer has since said he expects “double-digit billion” annual purchases of American agricultural goods over the next three years — roughly restoring the pre-2018 norm.

The deeper lesson is that farmers are increasingly dependent on diplomatic bargaining rather than open markets, powered by political favor rather than productive capacity or entrepreneurial initiative. China can punish, purchase, or redirect demand depending on relations with Washington. That makes domestic subsidies unavoidable.

According to the Government Accountability Office, USDA’s Market Facilitation Program provided $23 billion in 2018 and 2019, including $14.4 billion to about 644,000 operations, comprising more than 800,000 individuals. If Chinese purchases resume while subsidies remain, the result is not a restored free market but a but a narrower, more politicized one, with tariffs, subsidies, and politicians deciding who gets rescued.

The Multipolar Response

America’s turn toward managed rivalry forces other powers to insure themselves. As Washington redirects its attention toward China and the Indo-Pacific, Brussels can no longer assume that the old US-led order will organize global trade on its behalf. The result is not isolation, but bloc-building, with the EU–Mercosur and EU-India trade agreements leading the way.

The EU–Mercosur agreement began provisional application on May 1, 2026, linking the EU with Argentina, Brazil, Paraguay, and Uruguay, creating a trading zone of roughly 700 million people. The agreement supports European exporters by saving firms an estimated €4 billion in customs duties on goods such as car parts, machinery, chemicals, and pharmaceuticals, while also deepening EU access to Latin America’s agricultural products, minerals, and critical raw materials. This is why the European Commission has framed the Mercosur relationship not only as a trade deal, but as part of Europe’s strategy to secure resilient supply chains and reduce strategic dependence.

India offers Europe something Mercosur cannot: scale, services, manufacturing diversification, and Indo-Pacific leverage. After more than a decade of stop-start negotiations, the EU–India agreement is expected to double EU goods exports to India by 2032 and eliminate or reduce tariffs on 96.6 percent of EU goods exports. It is the EU’s most economically significant bilateral trade agreement ever, giving European firms deeper access to the world’s most populous country and one of the fastest-growing major economies.

Both agreements should be read as geopolitical insurance policies. Europe is not just lowering tariffs; it is securing supply chains, diversifying partners, and building leverage as the United States turns inward and toward Asia. These machinations are not “free trade.” They are negotiated corridors of access, hedged by rules, exceptions, quotas, and strategic objectives. Decades of negotiation, rules of origin, tariff schedules, environmental clauses, quotas, and ratification procedures show that the world is moving away from free trade.

French President Macron captured the logic clearly: “In the world we live in — with American tariffs and Chinese overcapacity — we must protect our production capacities.” He added that the objective is, “not to be the vessels of two hegemonic powers.” That is the language of bloc strategy. The “secondary” powers are fully aware of the changing status quo.

The Rise of Managed Globalization in a Multipolar World

Free trade has lost its innocence. The old promise was that open markets would soften rivalry and discipline governments. Instead, the United States tried to liberalize China through trade and found itself managing a powerful rival through tariffs, export controls, aircraft deals, farm purchases, investment boards, and subsidies. Brussels, seeing Washington turn inward and toward Asia, is building its own corridors with Mercosur and India.

This is not the end of globalization, but the end of globalization as a neutral, American-led project. Government intervention, introduced via tariffs, does not stop. Tariffs invite retaliation; retaliation invites subsidies; subsidies invite managed deals; and managed deals invite more bureaucracy. That is controlled commerce: trade still moves, but increasingly through political management rather than open exchange. The world is still trading. It has simply stopped pretending that trade is free from coercive power.